Background:

Eimco Elecon Limited (Eimco) is in the business of manufacturing & marketing of equipments for underground mines. It was incorporated in 1974 in Anand, Gujarat. Eimco has the largest market share in underground mining equipment industry in India.

Eimco was first to introduce intermediate technology of Side Dump Loaders (SDLs), Load Haul Dumpers (LHDs) & Rocker Shovel Loaders in India to partially mechanise the underground Coal and metal mines.

Eimco later introduced Face & Roof Drills, Coal Haulers, different models of LHDs / SDLs, etc. for underground mines. Eimco has also started manufacturing equipments for the construction segment.

LHD for Underground Mining

Mining Industry:

India has set itself an ambitious target of increasing coal production from 565.77 million tonnes in 2013-14 to 1.0 billion tonnes by ~2020 to reduce dependence on imports.

The most prevalent method of coal mining in India is opencast or surface mining, used for extracting coal deposits at shallow depths. Open cast mining is more efficient with average output (in tonnes) of 13 per man-shift; this output is just 0.8 in underground mines. Underground mining requires complex process and conveyor system to transport coal out. However, opencast mining affects the vegetation, soil and wildlife around the mine due to use of explosives. This adverse effect on environment straightens the case of underground mining. The coal quality from underground mining is also considered better than surface mining.

Contribution of underground mines in other major coal producing countries like China, USA and Australia are 95%, 30% and 25%, respectively. In India, this contribution has been going down and currently stands at around 8%. Government of India is expected to invest Rs 7.6 bn in the underground coal mines in FY2016. The share of underground mining should go up if India are to catch up with global averages.

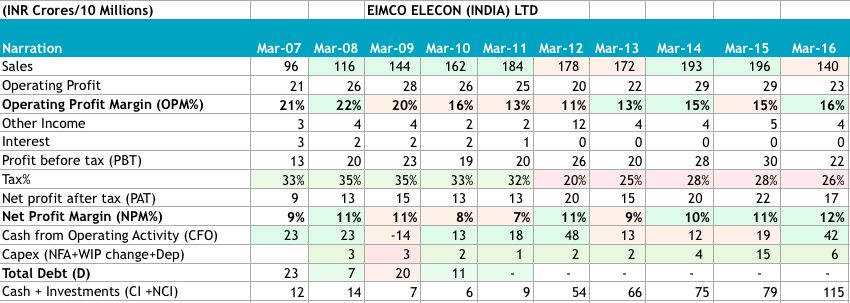

Financial Analysis:

Eimco did sales of INR 140 cr and net profit of INR 17 cr in FY2016. Eimco has shown muted CAGR of just 4% over last 10 years.

Sales dipped after FY2011; this reduction was due to sale of Surface Drilling Product Line to Sandvik Asia Pvt. Ltd. in FY2012 for a consideration of INR 16.5 cr. Sales improved after FY2012 but saw significant fall of ~28% in FY2016 over previous year. This drop was due to delay in orders by Coal India, which is Eimco’s major client. Operating & net margins have settled around healthy 15-16% and 10-11% respectively.

Eimco has cash and liquid investments of around INR 115 cr which is 48% of the current market cap.

Eimco has generated free cash flow of INR 160 cr over last 10 years. Free cash flow is around 81% of the cash flow from operations. Hence, Eimco was required to invest only 19% in the capex. Eimco’s business seems to be asset light given very low levels of capex requirements.

Turnover parameters took hit in FY2016. Receivable days are on the higher side indicating weak bargaining power of company with its clients. Public sector companies like Coal India can extract better payment terms from its suppliers.

Revenue Mix:

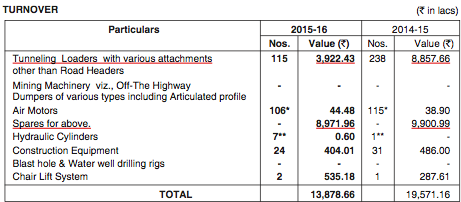

Eimco’s 65.0% revenue was generated from sale of spare parts and servicing of old equipments in FY2016. Once a machine is sold, Eimco locks in spare parts & servicing revenues for future. The spare business revenue was 51% in FY2015. This increase in spare parts share was due to reduction in revenue from sales of tunnelling loaders as compared to FY2015.

Eimco depends on Coal India for around 85% of its revenue. Management is trying to reduce dependence on Coal India by developing new products lines.

Management:

Mr. M.G. Rao is the whole time director since 2011. His renumeration was INR 79 lakhs in FY2016, a reduction of 18% as compared to reduction of 23% in profit after tax.

Mr. P. M. Patel is the chairman and promoter. Company’s board consists 4 independent directors and 3 executive director. Mr. P. M. Patel, Mr. H. S. Parikh and Mr. P. C. Amin are also on board of Elecon Engineering too, a related part of Eimco.

Board seems to be a coterie of experienced people; a minority shareholder may take some comfort from the board constitution.

Execution Capabilities:

Management has actively signed agreements with global players to bring in latest mining technology to India.

Management has remained pro-active in identifying needs of the market and launching products ahead of time. Eimco switched from intermediate technology to continuous technology; an opportunity which management identified in 2004. Management signed agreement with VoestAlpine for developing Continuous Miner ACM-10.

Similarly, management identified opportunity in construction equipment and engaged with Huta Stalowa in 2008 to develop Wheel Loader. Eimco first developed small loader of size 1.2 m3 in 2008 and launched a heavier version 1.9m3 in 2014 with some delay. Management mentioned unexpected reasons for this delay. Eimco launched heavier models of size 1.9-3.0 m3 in 2016.

Management efficiently launched Drill Machine product line. The trials started in 2009 and manufacturing in 2010. Eimco got the manufacturer status in 2011.

Eimco has launched Chair Lift Man Riding System (CLMRS) for the transportation inside the coal mines. Here is a quick youtube video explaining how this innovative system works.

Below is an excerpt from FY2016 annual report regarding launch of new product lines.

We shall also be introducing product, Skid Steer Loader, a highly versatile machine having a growth potential & primarily use in Industry material handling as well as infra projects. Also a line of action on recommendation from a reputed market survey agency, which conducted the market survey for us to add additional product lines in Construction Equipment Segment, will help your company realize its growth objective in years to follow.

Product Development Lifecycles:

Below table captures the main product lines and their development stages. This table helps in understanding how management changed its focus from intermediate technology to continuous mining technology and explored opportunities in construction equipment space. This table also captures management's though process of these product lines.

Shareholding:

Promoters hold around 48.9% shares at the end of FY2016. Of this, 16.62% shares are held through Eimco Engineering, a listed entity and 14.2% through Emtici Engineering. Eimco Engineering has pledged 9.9% of its shares to its lenders.

Tamrock Great Britain Holding, a subsidiary of Sandvik holds 25.1% shares. Sandvik bought the surface drilling business from Eimco in 2011. Sandvik is one of the largest players in mining equipment manufacturing space.

Mutual funds hold another 4.7% shares.

Contingent Liabilities:

Eimco has given lien on its mutual fund investments towards indebtedness of Elecon Engineering for INR 29.4 cr. An investor should consider liens as actual debt for the company. Eimco’s total equity is INR 218 cr; hence debt to equity will be just around 0.1, if lien is considered as debt.

Company may have outflow of INR 10 cr if it loses the excise duty dispute case. This is more than 50% of annual net profit.

Bank guarantees crystallise when company fails to provide machines/spare parts to its clients which is an operational risk. Investor should be concerned with non-operating contingent liabilities which, in case of Eimco, totals to INR 41.7 cr.

Valuation:

Let’s use the prudent banker approach to value Eimco.

Average CFO for Eimco Elecon over 5 years: Rs. 27 cr.

Cash & Investment in mutual funds/stocks at the end of FY2016: Rs. 115 cr.

A prudent banker will be comfortable lending to Eimco if CFO can comfortably cover the interest portion. Typically prudent banker wouldn’t want the interest burden to be more than 1/3rd of CFO. Hence, the annual interest expense should be upto Rs. 9 cr. Assuming an interest rate of 12%, max. loan value would be Rs. 75 cr.

If Eimco Elecon borrows Rs. 75 cr, the overall cash position will improve from Rs. 115 cr to Rs. 190 cr (115+75). Eimco Elecon has outstanding shares of 0.6 cr.

New cash & equivalent per share = (190 / 0.6) = Rs. 317

An investor should be delighted to buy Eimco shares if the share price is below Rs. 317 with serviceable debt on the books. Here, the underlying assumption is that Eimco Elecon will produce similar cash flows from operations as it did in last 5 years. Any improvement in CFO will increase the intrinsic value of the business.

Let’s also see in how many years, Eimco Elecon will be able to repay the loan.

Assuming PAT goes towards settling debt, Eimco will be able to repay the loan in 5 years.

Share price is hovering around INR 400-420. The price to earning ratio is around 14. Eimco seems fairly valued and any further movement in stock price should be accompanied by better off-take of its mining equipments.

Conclusion

Eimco is uniquely positioned to benefit from increased activity in mining sector. Government’s greater focus should increase the activity in underground mining space, which is way below the global average.

Eimco’s dependence on Coal India and its subsidiaries for majority of its revenue should be a cause of concern. However, management has shown intent to diversify its revenue base by launching new product lines.

Another important factor to watch out for will be how company uses the huge cash / cash equivalent pile of around INR 115 cr. Management has conserved cash so far by not wasting in ‘divorsification’; prudent use of this cash will decide the future of the company.

Disclaimer:

All data has been taken from public sources. I have financial interests in Eimco Elecon. I have purchased shares in last 15 days. My views may be biased about the company. This article is not a recommendation to buy or sell the stock; it's just collection of my thoughts about the company. An investor should do her own analysis before making an investment decision. Readers may also go through my portfolio to understand my direct / indirect interests in various businesses. The views expressed are personal and doesn't represent that of my employer’s.

I am not registered with SEBI under SEBI (Research Analysts) Regulations, 2014. As per the clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations.

Please refer to 'Disclaimer' page for further details.

Dear Vikrant, thank you for detailed review of Eimco. I'm particularly curious to learn if you are able to elaborate the receivable days that has steadily increased to 183 days in FY16. Apart from poor negotiation power with its customer, what other risks exist due to this deteriorating parameter - Shriram

ReplyDelete